When a DoorDash driver is involved in a crash, the first question isn’t "who’s at fault?" but "what insurance actually covers the damage?" From the moment the app pings you with a new order, you’re operating under a patchwork of policies that blend DoorDash’s own coverage with your personal auto insurance and, in some cases, provincial workers' compensation. The answer can feel like a maze, but breaking it down step‑by‑step makes it manageable.

Understanding DoorDash’s Insurance Policy

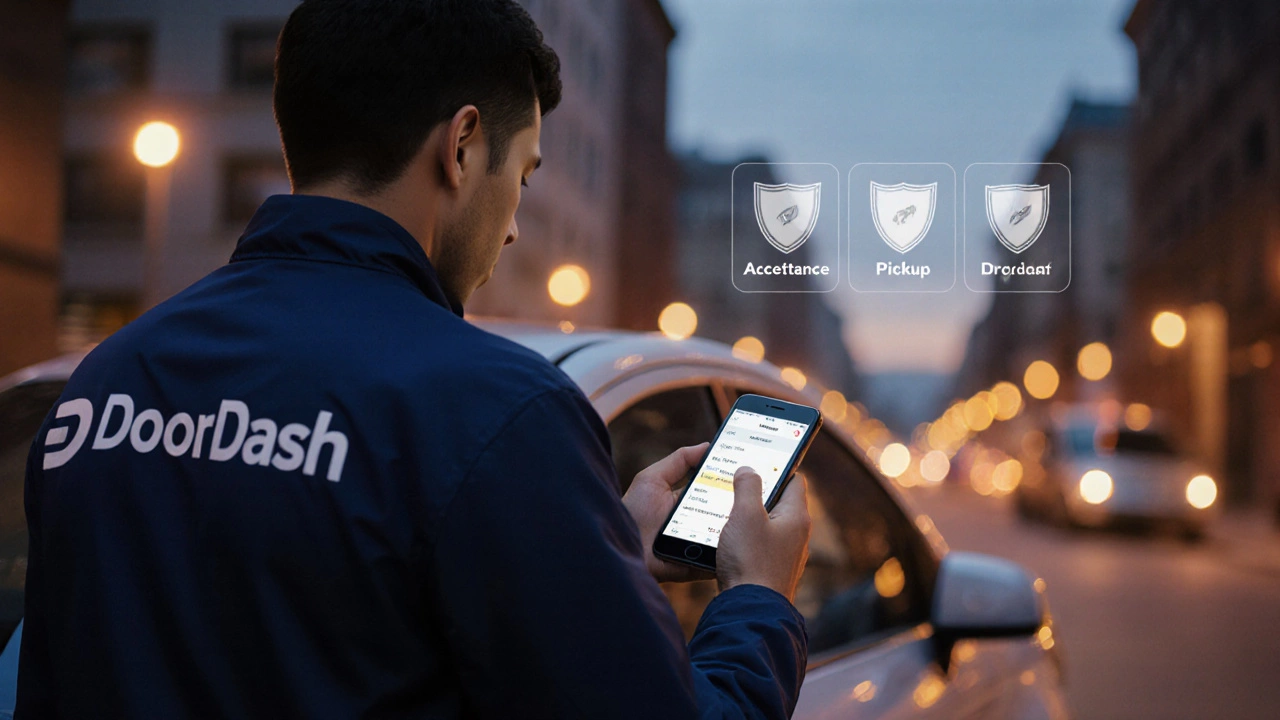

DoorDash provides three layers of coverage that kick in at different moments during a delivery:

- During the “App‑On” phase - when you have the app open but haven’t accepted a order yet - you’re covered only by your personal auto policy.

- Between “Acceptance” and “Pickup” - once you accept an order but haven’t reached the restaurant - DoorDash adds a limited liability policy (up to $50,000) for third‑party bodily injury and property damage.

- From “Pickup” to “Drop‑off” - the most critical window - DoorDash supplies a commercial auto policy that provides up to $1 million in liability, plus $250,000 for physical injury to the driver.

These layers are designed to fill gaps left by traditional personal policies, but they come with conditions. For example, the coverage only applies while you’re actively transporting a DoorDash order. If you take a detour for personal reasons, the protection could be void.

How Personal Auto Insurance Interacts

Most drivers think their own policy is the first line of defense, but that’s only true during the “App‑On” phase. Once you move into the delivery window, DoorDash’s commercial policy becomes primary, and your personal policy drops to secondary coverage - it steps in after DoorDash limits are exhausted.

Ontario’s Insurance Act (which also guides many other Canadian provinces) treats rideshare and gig‑delivery contracts similarly to rideshare services. This means your insurer may impose a “rideshare endorsement” or raise your premium if you regularly use the vehicle for DoorDash deliveries. Some insurers even refuse coverage unless you add a specific gig‑economy rider, which can add $75‑$150 to your annual premium.

Because of this overlap, many drivers end up paying two premiums: one for personal coverage and another for the DoorDash‑provided commercial policy (often baked into the platform’s fee). Knowing where each policy starts and stops saves you from surprise claim denials.

Steps to Take Right After an Accident

Reacting quickly and correctly can make the difference between a smooth claim and a legal nightmare. Follow this checklist:

- Ensure safety: Move to a safe spot if possible, turn on hazard lights, and check for injuries.

- Document the scene: Take photos of vehicle damage, road conditions, and any other parties involved. Capture the DoorDash order screen to prove you were in the delivery window.

- Exchange information: Get the other driver’s name, contact, insurance details, and license plate. Provide your own details, but note you’re a DoorDash driver.

- File a police report: In Ontario, a report is mandatory for collisions that cause damage over $2,000 or any injury. The report number is essential for insurance claims.

- Notify DoorDash: Use the driver app to report the incident immediately. The platform’s “Help” section guides you through uploading photos and the police report.

- Contact your personal insurer: Even though DoorDash’s policy is primary, letting your insurer know prevents gaps and helps them assess secondary coverage.

Skipping any of these steps can void coverage or delay payments, so treat each as non‑negotiable.

Filing a Claim with DoorDash

DoorDash’s claims process is digital‑first but still requires paperwork. Here’s how to move through it efficiently:

- Open the driver app: Tap the “📞 Help” icon, select “Report an Accident,” and upload all photos, police report, and order details.

- Provide a narrative: Write a concise, factual description of what happened. Stick to the timeline; avoid speculation about fault.

- Submit supporting documents: Include medical bills (if applicable), repair estimates, and any witness statements.

- Wait for the adjuster: DoorDash partners with a third‑party adjuster who will review the claim, contact you for clarification, and determine liability.

- Coordinate with your insurer: If the adjuster exhausts DoorDash’s limits, they’ll forward the claim to your personal insurer for secondary coverage.

Typical turnaround time in Canada is 10‑14 business days for straightforward cases. Complex claims involving multiple vehicles or severe injuries can take longer.

What Compensation Can Drivers Expect?

Compensation splits into three buckets:

| Coverage Type | Limit (CAD) | Primary/Secondary | Applies When |

|---|---|---|---|

| DoorDash Commercial Liability | $1,000,000 | Primary | Pickup → Drop‑off |

| DoorDash Limited Liability | $50,000 | Primary | Acceptance → Pickup |

| Personal Auto Liability | Varies (commonly $1,000,000) | Secondary | All other times |

| Personal Collision Coverage | Deductible $500‑$1,000 | Secondary | Any accident |

| Workers’ Compensation (Ontario) | Statutory benefits | Supplemental | In‑jury on the job |

When DoorDash’s liability hits its limit, your personal policy can pick up the slack, but only after you’ve met any deductibles. Injuries to the driver are typically covered under Workers’ Compensation in Ontario, which pays wage replacement and medical expenses regardless of fault.

In practice, drivers report receiving:

- Repair reimbursements ranging from $1,200 to $4,500, depending on vehicle make.

- Medical expense coverage that can reach $20,000 for minor injuries, with higher amounts for severe cases covered by workers’ comp.

- Lost‑time pay (usually 95% of average earnings) for up to 26 weeks under Ontario’s Workplace Safety and Insurance Board (WSIB).

These numbers vary by province, but the framework stays the same: DoorDash handles the bulk, personal policies fill gaps, and provincial workers’ comp protects the driver’s health.

Common Pitfalls and How to Avoid Them

Even seasoned drivers stumble into traps that jeopardize coverage:

- Driving off‑schedule: Taking a coffee break or a personal errand without marking yourself “off‑duty” in the app can invalidate DoorDash’s commercial policy.

- Missing the police report number: DoorDash’s adjusters often reject claims lacking a valid report, especially for damages over $2,000.

- Not informing your personal insurer: Some insurers consider undisclosed gig work a breach of contract, leading to policy cancellation.

- Assuming all injuries are covered by DoorDash: Only injuries that occur during the delivery window are covered by the platform’s policy. Slip‑and‑fall injuries while waiting at a restaurant fall back to personal or workers' comp.

- Delaying claim submission: Most policies have a 30‑day reporting window. Late filings can be rejected outright.

Keeping a simple log in your phone-date, order ID, mileage, and a quick note on whether you were on a personal detour-can save you a lot of headaches when an accident does happen.

Frequently Asked Questions

Does DoorDash cover damage to my own vehicle?

DoorDash’s commercial policy only covers liability to third parties. Collision or comprehensive damage to your own vehicle is paid by your personal auto insurance, after DoorDash’s liability limits are reached.

What if the other driver is at fault?

If the other driver’s insurance accepts responsibility, their liability coverage will handle repairs and medical bills. DoorDash’s policy still steps in if the other driver is uninsured or under‑insured, up to its limits.

Do I need a special rideshare endorsement on my personal policy?

Many Canadian insurers now require a gig‑economy rider for delivery work. It typically adds $75‑$150 per year. Without it, you risk a denial of secondary coverage.

How long does a DoorDash claim take?

For straightforward accidents, expect 10‑14 business days. Complex cases involving multiple parties can stretch to 30‑45 days.

Can I continue delivering while my claim is processing?

Yes, as long as your vehicle is drivable and you remain within DoorDash’s coverage window. If your car needs repairs, you may need a rental or use a backup vehicle.

Understanding the layers of insurance, acting fast, and keeping clear records are the three pillars that turn a scary crash into a manageable claim. With the right knowledge, a DoorDash driver can protect their earnings, their car, and their health without getting tangled in paperwork.